How to Compare Insurance Plans Like a Pro

The smart way to compare insurance plans and avoid costly mistakes—whether you're shopping for health, auto, or home coverage.

How to Compare Insurance Plans Like a Pro

Americans waste $37 billion annually on the wrong insurance policies. Here's how to avoid being part of that statistic.

Comparing insurance plans isn't just about finding the cheapest option—it's about matching coverage to your actual needs. We'll walk you through the key factors professionals use to evaluate policies, from hidden exclusions to claim satisfaction rates. You'll learn how to compare apples to apples, whether you're shopping for health, auto, home, or life insurance.

Insurance Comparison—What It Is and Why It Matters

Insurance comparison is the process of evaluating multiple policies side-by-side using standardized metrics like coverage limits, exclusions, premiums, and provider reputation. Unlike simple price shopping, true comparison weighs both cost and protection quality to find the optimal balance for your specific situation.

With insurance premiums rising faster than inflation—health insurance costs jumped 47% over the past decade—making smart comparisons is more crucial than ever. The right evaluation can save you thousands annually while ensuring you're actually protected when disaster strikes.

Why This Is Important Right Now

Open enrollment periods for health insurance create urgent decision windows. Auto insurance rates just hit record highs in 37 states. And climate change has rewritten the rules for homeowners coverage in disaster-prone areas.

Consider Sarah from Florida, who saved $1,200/year by switching home insurers—only to discover her new policy excluded hurricane damage two weeks before Ian hit. Proper comparison would have flagged that critical gap.

Key Facts About Insurance Comparison

These five principles separate savvy insurance shoppers from those who overpay or end up underinsured:

- Premiums tell half the story — A policy with 20% lower premiums but 50% higher deductibles might cost more when you actually need coverage

- Insurers calculate risk differently — Your driving record might matter more to one auto insurer while another weighs credit score heavier

- Network size impacts value — Health insurance with 10% more doctors in-network often provides better real-world access than a slightly cheaper plan

- Financial ratings matter — An AM Best A-rated insurer is 83% less likely to dispute claims than a B-rated competitor

- Discounts aren't equal — Bundling auto+home might save 15% with one provider but only 8% with another

What the Industry Data Shows

Industry analysis consistently shows most consumers focus too narrowly on premium prices. Research suggests 62% of policyholders couldn't accurately state their deductible amounts, and 41% weren't aware of key exclusions in their coverage.

The most valuable comparison tools go beyond simple rate quotes. They analyze how often insurers approve claims, customer satisfaction with payout amounts, and dispute resolution timelines—factors that matter most when you actually need your insurance.

Benefits and Real Opportunities

Proper insurance comparison delivers measurable financial and security advantages:

- Lower total costs — Balancing premiums with deductibles and copays can save $500+/year on average

- Better claims experience — Some insurers approve claims 40% faster than competitors in the same price range

- Tailored coverage — You avoid paying for protections you don't need while ensuring critical risks are covered

- Future-proofing — Identifying insurers with stable rates helps avoid surprise premium hikes

Costs and What to Expect

While comparison shopping takes 2-3 hours initially, the payoff justifies the time. Many consumers find 15-30% savings on equivalent coverage. Independent agents often provide free comparison services—they earn commissions from insurers, not you.

Watch for these cost factors: Tiered pricing where your credit score affects rates, mileage thresholds on auto policies, and health insurance metal tiers (Bronze, Silver, Gold) that shift cost-sharing percentages.

Health vs Auto vs Home Insurance: Which Comparison Approach Works Best?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Health Insurance | Chronic conditions or planned procedures | Network quality matters most; easy to compare via Healthcare.gov | Limited enrollment windows; complex benefit structures |

| Auto Insurance | High-mileage drivers or those with accidents | Easy to get multiple quotes online; discounts widely available | Credit score impacts rates in most states |

| Home Insurance | Disaster-prone areas or high-value homes | Can customize coverage precisely; bundling saves significantly | Exclusions vary wildly by provider and location |

Who Should Actually Care About Insurance Comparison?

If you're facing any life change—new job, new home, new driver in the family—it's time to compare. Also critical for those who haven't shopped policies in 3+ years, as insurer risk models and discount structures evolve constantly.

Mistakes Most People Make

These common errors cost Americans billions annually:

Focusing only on price

Cheapest plans often have the highest out-of-pocket costs when you need care or repairs. Always compare the total cost scenario.

Ignoring provider stability

An insurer with slightly higher rates but strong financials is less likely to hike premiums abruptly or fight claims.

Overlooking policy changes

Insurers frequently adjust coverage terms. That flood protection you had last year might be gone now.

What Most Articles Won't Tell You

Insurers price policies based on secret "sweet spots." One might offer best rates to teachers while another prefers engineers. Independent agents know these patterns and can match you accordingly.

Also, claim satisfaction often correlates with insurer size—but inversely. Midsize regional insurers frequently outperform national giants on claim handling.

Advanced Moves Worth Knowing

Request your CLUE report (for auto/home) or MIB report (for health/life) before shopping. These show your insurance history and help avoid rate hikes based on errors.

For homeowners, ask about "replacement cost" vs "actual cash value" calculations. The difference could leave you six figures underinsured after a disaster.

Frequently Asked Questions

How often should I compare insurance policies?

Annually for auto and home insurance. Health insurance comparisons make sense during open enrollment or after life changes. Life insurance needs reassessment every 3-5 years or after major financial changes.

Will comparing rates hurt my credit score?

Auto and home insurance quotes typically trigger soft credit inquiries that don't affect your score. Multiple hard inquiries within 14-45 days (varies by state) often count as a single inquiry.

What's more important—premium or deductible?

It depends on your cash flow and risk tolerance. Low deductibles mean higher premiums but less out-of-pocket when claims happen. Run break-even calculations based on your claim history.

Can I trust online insurance comparison tools?

They're useful for initial rate comparisons but often miss insurer-specific discounts or coverage nuances. Follow up with direct quotes from shortlisted providers.

How do I compare insurers' claim satisfaction?

Check NAIC complaint ratios, J.D. Power ratings, and your state's insurance department website. Look for patterns in how insurers handle claims like yours.

The Bottom Line on Insurance Comparison

Smart insurance comparison protects both your wallet and your future. By focusing on total value rather than just premiums, you gain confidence that your coverage will deliver when needed most. Set aside two hours this week to review your policies—that small investment could save you thousands this year while ensuring you're truly protected.

Read Next

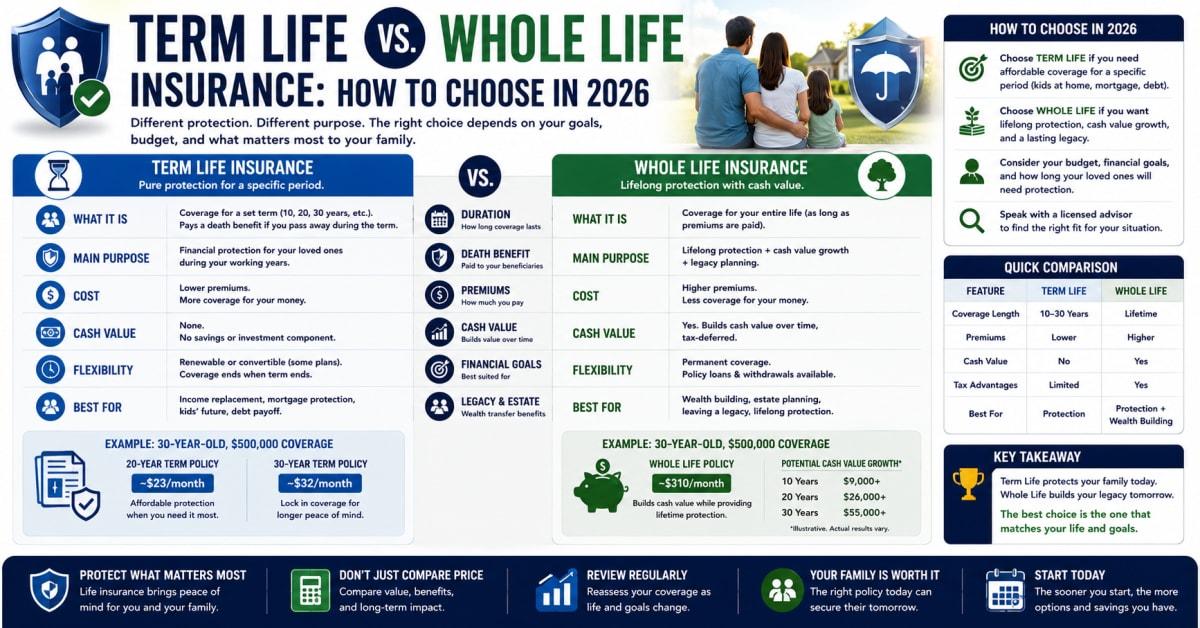

Term Life vs Whole Life Insurance: How to Choose in 2026

Roth IRA vs 401(k): Which Wins for You in 2026?

Pet Insurance in 2026: Is It Worth It for Dogs and Cats?

How Much Life Insurance Do You Need? 2026 Calculator Guide

Government Health Insurance in Australia Explained