Term Life vs Whole Life Insurance: How to Choose in 2026

Whole life costs 5-15 times more than term for the same death benefit. Here's when that extra cost is actually worth it, and when it isn't.

Term Life vs Whole Life Insurance: How to Choose in 2026

Two people can buy the exact same $500,000 death benefit, and one pays five to fifteen times more per month than the other. That gap isn't a scam. It's the price difference between temporary and permanent coverage, and most people never fully understand it before buying.

Choosing between term life and whole life insurance in 2026 comes down to understanding what you're actually paying for beyond the death benefit itself. This guide breaks down the real cost difference, where each policy type genuinely makes sense, and how to avoid the most common mistake: buying permanent coverage for a need that's actually temporary.

Term Life vs Whole Life Insurance — What They Are and Why the Difference Matters

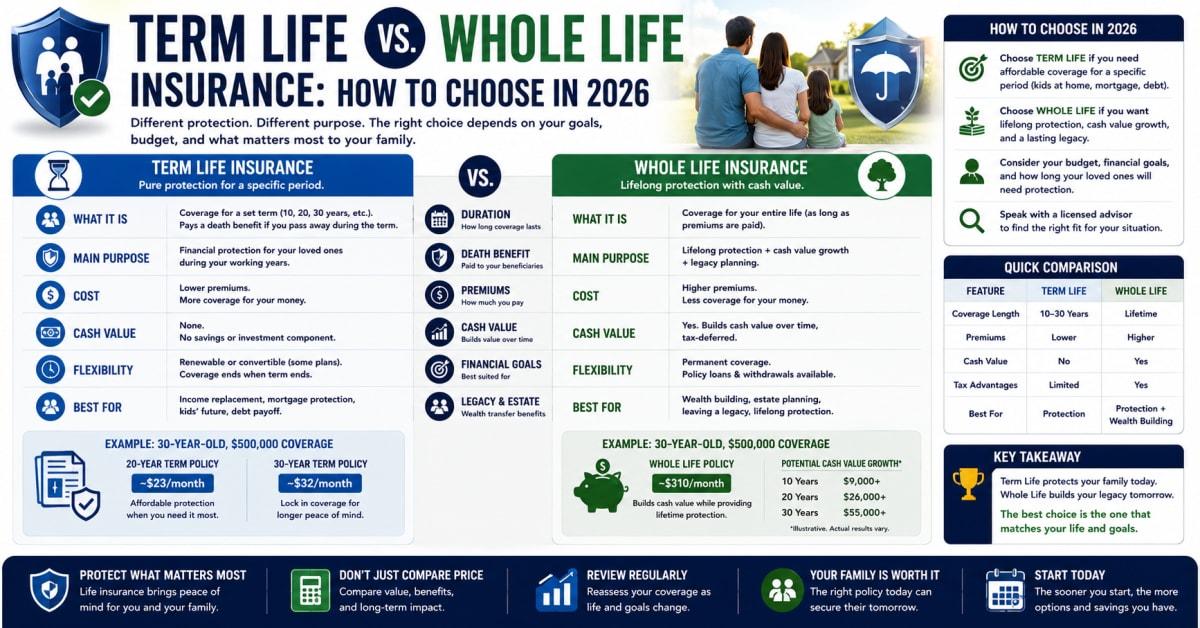

Term life insurance provides coverage for a fixed period, commonly 10, 20, or 30 years, and pays a death benefit only if you pass away during that term. Whole life insurance provides coverage for your entire life, as long as premiums are paid, and includes a cash value component that grows over time and can be borrowed against.

This distinction matters because it changes not just the cost, but the entire purpose of the policy. Term life is pure protection for a specific window of time, while whole life combines protection with a savings and investment element that carries its own costs and tradeoffs.

Why This Is Important Right Now

Picture a parent buying whole life insurance to cover a 25-year mortgage, paying several times more per month than a term policy would cost for the same death benefit, without realizing the mortgage itself will be paid off well before "whole life" coverage would ever be needed for that specific purpose.

With household budgets tighter than they've been in years for many families, the cost gap between term and whole life has become a more consequential decision than ever. Overpaying for permanent coverage tied to a temporary need quietly strains a budget that could be funding other goals instead.

Key Facts About Term Life vs Whole Life Insurance

A few core facts explain why these two policy types differ so dramatically in cost and purpose.

- Whole life premiums typically run five to fifteen times higher than term life — for the same death benefit amount and similar applicant profile.

- Term life has no cash value component — if you outlive the term, the policy simply ends with no payout, unless you convert or renew it.

- Whole life cash value grows slowly in early years — a significant portion of early premiums covers insurance costs and fees before meaningful cash value accumulates.

- Term policies often include a conversion option — allowing you to convert some or all of the coverage to a permanent policy later without new medical underwriting.

- Whole life dividends aren't guaranteed on many policies — some policies pay dividends based on the insurer's performance, but these aren't a contractual guarantee unless the policy specifically states otherwise.

What the Industry Data Shows

Industry data suggests that term life insurance remains the far more commonly purchased policy type among younger families, largely because it aligns with temporary financial obligations like a mortgage or the years until children reach financial independence.

Financial planning coverage in outlets like Forbes and NerdWallet has consistently noted that whole life insurance tends to make the most sense for people who have already maxed out other tax-advantaged savings vehicles and have a specific permanent need, such as estate planning or providing for a dependent with lifelong care needs, rather than as a primary savings strategy.

Benefits and Real Opportunities

Each policy type offers real, distinct advantages depending on what you're actually trying to accomplish.

- Term life maximizes coverage per dollar — you can typically afford a much larger death benefit for the same premium compared to whole life.

- Whole life provides lifelong certainty — coverage never expires as long as premiums are paid, which matters for permanent needs like a dependent with lifelong care requirements.

- Whole life cash value can be borrowed against — offering a source of funds in an emergency, though any unpaid loan reduces the eventual death benefit.

- Term conversion options provide flexibility — letting you lock in permanent coverage later without new medical underwriting, if your needs change.

Costs and What to Expect

A healthy applicant in their 30s can often secure a substantial 20-year term policy for a relatively modest monthly premium, sometimes under $30 for a $500,000 death benefit depending on health and coverage amount. A comparable whole life policy with the same death benefit can easily run several hundred dollars per month for that same applicant, reflecting the added cost of lifelong coverage and the built-in cash value component.

Whole life policies also often carry additional fees beyond the base premium, including administrative charges and surrender fees if you cancel the policy in its early years, which can significantly reduce the cash value you'd actually receive if you exit the policy early. Term life policies typically carry no such fees, since there's no cash value to manage, though renewing a term policy after it expires usually comes at a substantially higher premium reflecting your older age at that point.

Riders on either policy type, like a disability waiver of premium or an accelerated death benefit, typically add a modest amount to the premium but can provide valuable additional protection depending on your circumstances.

Term Life vs Whole Life vs Term With Conversion Option: Which One Is Right for You?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Term Life | Families with temporary obligations like a mortgage or dependent children | Much lower premium for a larger death benefit | Coverage ends with no payout if you outlive the term |

| Whole Life | People with a permanent need, like estate planning or lifelong dependents | Lifelong coverage with a growing cash value component | Significantly higher premium with slow early cash value growth |

| Term With Conversion Option | People wanting affordable coverage now with flexibility later | Lets you convert to permanent coverage later without new medical underwriting | Conversion typically must happen within a specific window or before a certain age |

Who Should Actually Care About This Decision?

This matters for anyone with a mortgage, dependent children, or other obligations tied to a specific timeframe, since term life is typically the more cost-effective match for those needs. It's also relevant for high-net-worth individuals focused on estate planning, and families with a dependent who will require lifelong financial care, since whole life's permanent structure genuinely fits those specific situations.

Mistakes Most People Make

A handful of errors show up repeatedly in this decision.

Buying whole life insurance primarily as a savings vehicle overlooks that the fees and slow early cash value growth often make it a weaker savings tool than simply maxing out a retirement account first. Treating whole life as insurance with a savings feature, not a primary investment strategy, sets more realistic expectations.

Choosing a term length shorter than your actual obligation, like a 10-year term for a 20-year mortgage, defeats the purpose of matching coverage to your real timeline. Calculating your actual obligation length before selecting a term avoids that mismatch.

Letting a whole life policy lapse in its early years, when surrender fees are highest, can mean losing a significant portion of the cash value you've built up. Understanding the surrender fee schedule before committing helps you assess whether you can realistically maintain the policy long term.

Assuming term life insurance is a poor value because "you get nothing back" if you outlive it misunderstands its purpose. Term life is pure protection for a specific risk window, similar to auto insurance, not an investment expected to pay out regardless.

What Most Articles Won't Tell You

Most comparisons present this as term versus whole life as if they're mutually exclusive, but laddering multiple term policies with different lengths, one matching your mortgage and another matching your years until retirement, often provides more precisely matched, cost-effective coverage than either extreme alone.

There's also a detail often missed: the conversion option built into many term policies is time-limited, often expiring by a certain age or policy year, so if you think you might eventually want permanent coverage, it's worth confirming your specific conversion window rather than assuming it stays available indefinitely.

Advanced Moves Worth Knowing

Laddering term policies of different lengths to match different obligations, rather than buying one large policy for your longest need, can lower your total premium cost while still covering every stage of your financial timeline.

If a genuine permanent need exists, comparing whole life against other permanent policy types, like universal life, before committing can reveal a structure that better fits your specific goals, since not all permanent insurance works identically.

Frequently Asked Questions

Is whole life insurance ever a good investment?

It can serve a role for people who've already maxed out other tax-advantaged accounts and have a specific permanent need, but the fees and slow early cash value growth generally make it a weaker pure investment vehicle compared to dedicated retirement or brokerage accounts.

What happens if I outlive my term life insurance policy?

The policy simply ends with no payout, unless you convert it to permanent coverage or renew it, typically at a much higher premium reflecting your older age at that point.

Can I convert a term life policy to whole life later?

Many term policies include a conversion option allowing you to switch some or all of the coverage to permanent insurance without new medical underwriting, though this option is usually only available within a specific window or before a certain age.

Why is whole life insurance so much more expensive than term?

Whole life covers you for your entire lifetime rather than a fixed term, and it includes a cash value savings component, both of which add significant cost compared to term life's pure, temporary protection.

How do I decide how long a term life policy I need?

Match the term length to your longest financial obligation, such as your remaining mortgage term or the number of years until your youngest child reaches financial independence, rather than choosing an arbitrary round number.

The Bottom Line on Term Life vs Whole Life Insurance in 2026

For most people, term life insurance offers far more coverage per dollar and matches the temporary nature of obligations like a mortgage or raising children. Whole life insurance genuinely earns its higher cost only for specific permanent needs, like estate planning or a lifelong dependent, not as a general-purpose savings strategy. Calculate your actual obligation length before choosing a term, and be honest about whether a permanent need truly exists before paying five to fifteen times more for whole life coverage you may not need for life at all.

Read Next

Shocking Surge: AARP Reveals New Medicare Caregiver Training Services Impact

Shocking Medicare Surprises Await Americans Working at 65—Are You Prepared?

Shocking Collapse: Ex-Ole Miss Star Gets 16 Years for $110M Medicare Fraud

Warning: Medicare Advantage Auto-Enrollments Could Lead to Financial Crisis for Seniors!

Shock Alert: Enroll in Medicare Now to Avoid Costly Crisis at 65!