Build a 6-Month Emergency Fund Faster in 2026

Saving six months of expenses feels impossible until you break it into the right accelerators. Here's how to actually speed up the timeline.

Build a 6-Month Emergency Fund Faster in 2026

A six-month emergency fund sounds like a multi-year project for most people, and for many, it is. But the gap between "eventually" and "in under a year" usually comes down to a handful of specific accelerators most people never try.

If you already understand why an emergency fund matters and you're past the basics, this guide skips straight to what actually speeds up the timeline. We'll cover the income and expense levers that make the biggest difference, the account structure that maximizes growth without sacrificing access, and the mistakes that quietly slow people down without them realizing it.

Building a 6-Month Emergency Fund Faster — What It Actually Takes

Speeding up a six-month emergency fund isn't about extreme frugality alone. It's about combining a few specific accelerators, temporary expense cuts, one-time windfalls, side income, and smarter account structure, so the fund grows faster than what a single monthly transfer could achieve on its own.

This matters because the standard advice to "just save more each month" often isn't fast enough on its own for people who want real protection sooner rather than in two or three years.

Why This Is Important Right Now

Picture someone with a $1,000 starter fund already in place, comfortable but still exposed to a job loss or a major medical bill. Sticking with the same $100-a-month pace that built the first $1,000 would take years to reach a full six-month cushion.

With layoffs and economic uncertainty still a real concern for many households in 2026, the difference between a one-year and a three-year timeline to full protection matters more than it might have in calmer economic periods.

Key Facts About Accelerating Your Emergency Fund

A few core principles separate a fund that builds quickly from one that crawls along at the same slow pace for years.

- Windfalls close the gap faster than monthly budgeting alone — tax refunds, bonuses, and cash gifts redirected in full can cut months off your timeline in a single deposit.

- Temporary lifestyle cuts work better than permanent ones — a defined, time-limited "savings sprint" is easier to sustain than an indefinite austerity budget.

- Side income accelerates the fund without touching your core budget — dedicating 100% of freelance or gig income to savings avoids lifestyle inflation eating into the progress.

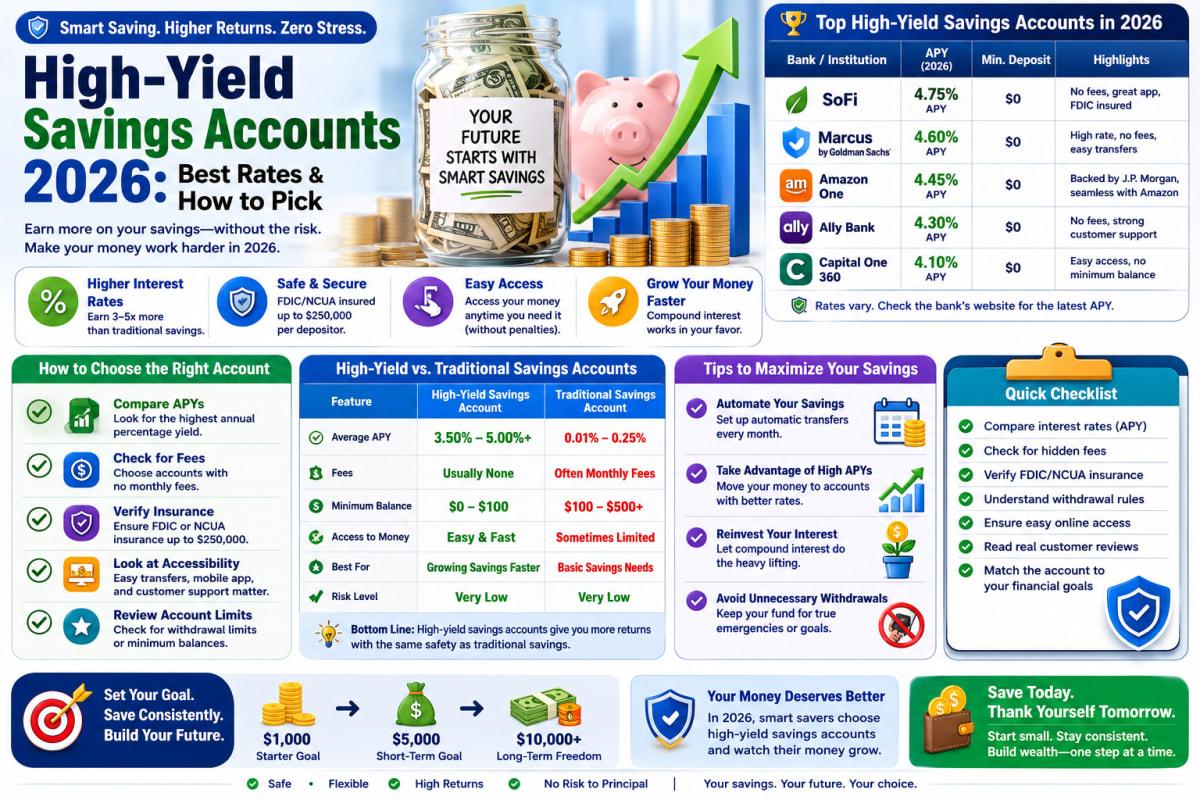

- A high-yield savings account meaningfully speeds up growth — the interest gap between a top-rate account and a traditional bank compounds noticeably over a year or two.

- Recalculating your actual target lowers the finish line — six months of essential expenses, not six months of your full current spending, is often a smaller number than people assume.

What the Industry Data Shows

Industry data suggests that households who direct windfalls like tax refunds toward savings goals build emergency funds significantly faster than those relying solely on incremental monthly contributions, since a single refund can often equal several months of typical savings progress.

Financial behavior research covered in outlets like Forbes and Bankrate has also found that clearly defined, time-limited savings challenges tend to outperform open-ended budget cuts, since a visible end date makes short-term sacrifice easier to sustain.

Benefits and Real Opportunities

Reaching a full six-month cushion faster creates real advantages beyond simply hitting the number sooner.

- Protection during the exact window you're most vulnerable — a faster timeline means less time exposed to a gap in coverage.

- More motivation to keep going — visible progress from windfalls and side income tends to build momentum that a slow, incremental pace doesn't.

- Freedom to redirect savings sooner — reaching your target faster means you can shift focus to other goals, like investing, that much sooner.

- Less total time carrying financial anxiety — a shorter runway to full protection reduces the cumulative stress of feeling underprepared.

Costs and What to Expect

There's no direct cost to accelerating your emergency fund beyond the temporary lifestyle adjustments you choose to make. A focused savings sprint might mean cutting discretionary spending by a meaningful percentage for three to six months, which is far more sustainable than attempting the same cuts indefinitely.

A high-yield savings account, the recommended home for this money, typically carries no monthly fee and no minimum balance at the most competitive providers, so switching accounts to maximize interest costs nothing beyond a few minutes of setup. Side income sources, like freelance work or selling unused items, may involve minor costs, such as platform fees on resale marketplaces, typically a small percentage of the sale price.

The real "cost" of an accelerated timeline is short-term sacrifice, temporarily reduced discretionary spending or extra hours worked, in exchange for reaching financial protection significantly sooner.

Windfall Redirection vs Temporary Budget Sprint vs Side Income Dedication: Which Accelerator Should You Prioritize?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Windfall Redirection | Anyone expecting a tax refund, bonus, or one-time payment | Large, immediate progress with zero lifestyle change required | Only works when a windfall is actually available |

| Temporary Budget Sprint | People with discretionary spending room to trim short-term | Doesn't require extra income, just short-term reallocation | Requires discipline to sustain even for a defined period |

| Side Income Dedication | People with time available for freelance or gig work | Adds new money without touching your existing budget | Requires available time and energy outside your main job |

Who Should Actually Care About Accelerating Their Emergency Fund?

This matters most for people who already have a starter fund, like $500 to $1,000, and want to push toward a full six-month cushion faster than their current pace allows. It's especially relevant for anyone in an industry facing layoff risk, freelancers with variable income who feel the gap more acutely, and households who recently experienced a near-miss financial scare that made the urgency real.

Mistakes Most People Make

A handful of habits slow down what could otherwise be a much faster timeline.

Spending a tax refund or bonus on discretionary purchases instead of redirecting it toward savings misses one of the single fastest accelerators available. Deciding in advance to send a set percentage of any windfall straight to savings removes the temptation once the money actually arrives.

Attempting an indefinite, extreme budget cut instead of a defined savings sprint often leads to burnout and abandoning the plan altogether. Setting a specific end date, like three months, makes short-term sacrifice far easier to sustain.

Letting side income blend into everyday spending instead of routing it directly to savings erodes the acceleration effect entirely. Automatically transferring side income to your emergency fund the moment it's received keeps it from disappearing into daily spending.

Keeping the fund in a low-interest traditional savings account throughout the entire process leaves meaningful interest on the table. Moving to a high-yield account early in the process compounds that advantage over the full timeline.

What Most Articles Won't Tell You

Most guides treat every month of savings as equally important, but front-loading windfalls and side income early in your timeline matters more than spreading contributions evenly, since money saved sooner has more time to earn interest before you'd need it.

There's also a detail worth knowing: recalculating your actual six-month target based on essential expenses only, not your full current spending including discretionary categories, often reveals a smaller finish line than people assume, which can meaningfully shorten the perceived distance left to go.

Advanced Moves Worth Knowing

Running a focused 90-day savings sprint, cutting discretionary spending aggressively but only for that defined window, can produce a meaningful lump sum without the burnout risk of an open-ended austerity budget.

Selling unused items around your home and routing that cash directly to your emergency fund, rather than letting it sit in a general checking account, adds a quick, one-time boost that many people overlook entirely.

Frequently Asked Questions

How fast can you realistically build a 6-month emergency fund?

The timeline varies widely based on income and expenses, but combining consistent monthly savings with windfalls and side income can realistically compress a multi-year timeline into twelve to eighteen months for many households.

Should I use my tax refund for my emergency fund or something else?

If you haven't reached a full emergency fund yet, redirecting most or all of a tax refund there is one of the most effective single accelerators available, since it adds a lump sum without requiring any change to your monthly budget.

Is it better to do a short, intense savings sprint or a longer, gentler pace?

A defined, time-limited sprint, such as ninety days of aggressive saving, tends to be more sustainable than an indefinite austerity budget, since a visible end date makes the temporary sacrifice easier to commit to fully.

Does the interest rate on my savings account really make a difference for a shorter timeline?

Yes, even over twelve to eighteen months, the gap between a top high-yield rate and a traditional bank's rate adds up to a meaningful amount, especially as your balance grows throughout the process.

Should I pause retirement contributions to build my emergency fund faster?

If your employer offers a matching contribution, most financial guidance recommends still capturing that match, since it's essentially free money. Beyond the match, temporarily reducing extra retirement contributions to accelerate an emergency fund can be a reasonable short-term tradeoff for many households.

The Bottom Line on Building a 6-Month Emergency Fund Faster

Reaching a full six-month cushion faster isn't about willpower alone. It's about stacking a few specific accelerators, windfall redirection, a defined savings sprint, and side income dedication, on top of your regular monthly contributions. Recalculate your actual target based on essential expenses, move your savings into a high-yield account early, and commit your next windfall to the fund before it has a chance to get spent elsewhere. The households that get there fastest aren't the ones earning the most. They're the ones who stop letting extra money quietly disappear.

Read Next

Money Market vs High-Yield Savings: Which Wins in 2026?

7 Proven Budgeting Methods That Actually Work in 2026

How to Create a Monthly Budget That Actually Works

Best Checking Accounts in 2026: Fees, Rewards Compared

High-Yield Savings Accounts 2026: Best Rates & How to Pick