7 Proven Budgeting Methods That Actually Work in 2026

Seven proven budgeting methods, compared side by side, so you can pick the one that actually matches your personality instead of guessing.

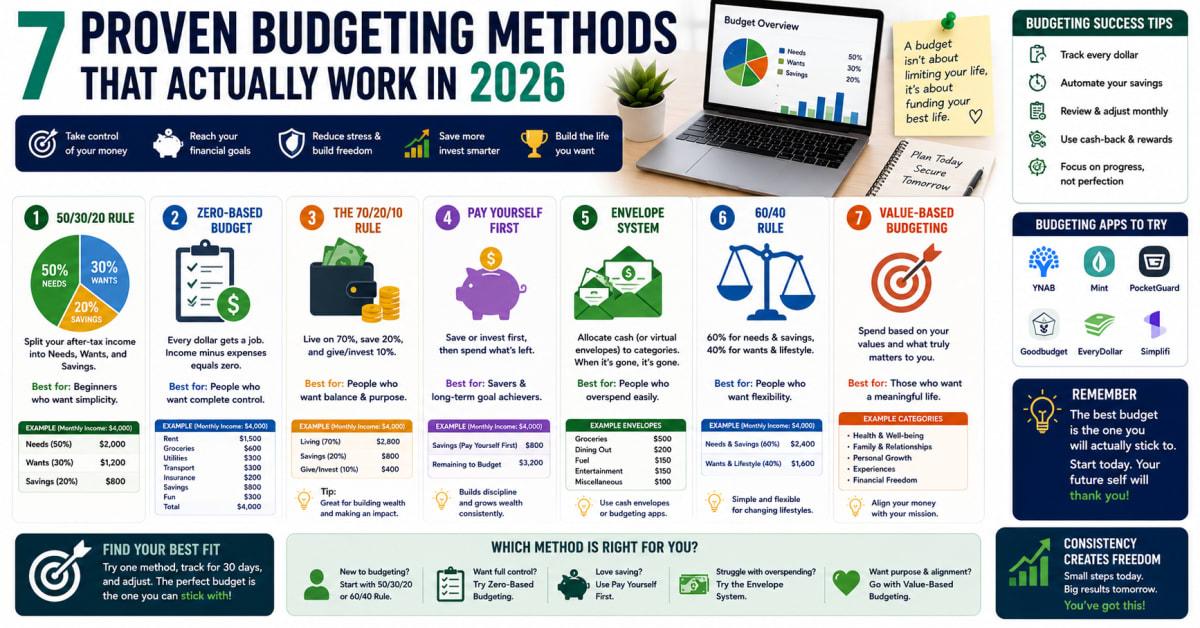

7 Proven Budgeting Methods That Actually Work in 2026

There's no single "best" budgeting method, only the one you'll actually keep using past the first month. The right fit depends far more on your personality than on which system is theoretically most efficient.

This guide breaks down seven proven budgeting methods used in 2026, from strict zero-based budgeting to more flexible, automation-driven approaches. Instead of picking one and hoping it fits, you'll see exactly who each method suits best, so you can choose with confidence the first time instead of cycling through apps that never stick.

Budgeting Methods — What They Are and Why the Right Fit Matters

A budgeting method is simply a structured system for deciding where your money goes each month. Some methods assign every dollar a specific job, others work with broad percentage targets, and some rely almost entirely on automation instead of manual tracking.

Choosing the wrong method for your personality is the single biggest reason budgets get abandoned. Someone who hates detailed tracking will quit a zero-based budget within weeks, while someone who needs firm limits will find a loose percentage-based system too vague to actually change their behavior.

Why This Is Important Right Now

Picture someone who's downloaded and abandoned three different budgeting apps in the past year, each time blaming themselves for lacking discipline. In most cases, the real issue wasn't willpower. It was using a method built for a different kind of person entirely.

With more budgeting tools and methods available than ever in 2026, the paradox of choice has made it harder, not easier, to settle on one system. Understanding the real differences between methods upfront saves months of trial and error.

The 7 Budgeting Methods, Compared

Each of these methods solves the budgeting problem differently, and none of them is objectively better across the board. The right one depends entirely on your specific habits and preferences.

- Zero-based budgeting — Every dollar of income is assigned a specific category, so income minus expenses always equals zero. Best for detail-oriented planners who want maximum control.

- 50/30/20 budgeting — Splits income into needs, wants, and savings using broad percentage targets. Best for beginners who want structure without granular tracking.

- Envelope budgeting — Cash or digital "envelopes" hold a fixed amount per category, and spending stops once an envelope is empty. Best for people who overspend easily with cards.

- Pay-yourself-first budgeting — Savings and investments are automated immediately after each paycheck, and remaining money is spent freely. Best for people who prioritize long-term goals over detailed tracking.

- The 6-jar method — Income is split across six purpose-driven categories, including necessities, savings, education, and giving, each with a fixed percentage. Best for people wanting a values-driven structure beyond just needs and wants.

- Reverse budgeting — Similar to pay-yourself-first, but emphasizes automating every fixed obligation, not just savings, so only true discretionary spending requires active decisions. Best for people who want budgeting to feel nearly invisible.

- App-based automatic budgeting — Software automatically categorizes transactions and flags overspending in real time. Best for tech-comfortable users who want tracking without manual data entry.

Key Facts About Choosing a Budgeting Method

A few core principles help explain why matching the method to your personality matters more than picking the "best" one in the abstract.

- Consistency beats precision — a simple method followed every month outperforms a detailed one abandoned after six weeks.

- Automation reduces reliance on willpower — methods that automate savings and bill payments tend to survive busy or stressful months better than fully manual systems.

- Rigid methods work best for people who like rules — zero-based and envelope budgeting suit people who find firm boundaries motivating rather than restrictive.

- Flexible methods work best for people who resent tracking — pay-yourself-first and reverse budgeting suit people who want results without daily categorization.

- Most methods can be combined — pairing pay-yourself-first automation with a loose 50/30/20 framework for the rest is a common and effective hybrid.

What the Industry Data Shows

Industry data suggests that budgeting methods emphasizing automation over manual tracking tend to see stronger long-term adherence, since they remove the daily decision fatigue that causes many people to abandon a system within the first few months.

Financial behavior coverage in outlets like NerdWallet and Forbes has consistently noted that no single method outperforms the others universally. Success correlates far more strongly with matching the method to the individual's personality and existing habits than with any inherent superiority of one system over another.

Benefits and Real Opportunities

Picking the right method for your specific personality creates real, lasting benefits that a mismatched system never delivers.

- Higher long-term adherence — a method that fits your habits is far more likely to still be in use a year from now.

- Less financial stress — a system that doesn't feel like a fight against your own nature reduces the anxiety often associated with budgeting.

- Faster progress toward goals — consistency, even with a simple method, compounds into real savings and debt payoff over time.

- Room to evolve — starting with a simpler method and adding structure later is easier than starting too rigid and burning out.

Costs and What to Expect

Every method described here can be implemented entirely for free using a spreadsheet, a notebook, or your bank's existing tools. Many people choose to pair a method with a budgeting app for convenience, and free app tiers typically cover basic tracking, while premium tiers with automatic categorization or shared household access commonly run $5 to $15 per month.

Envelope-based systems using physical cash carry no software cost at all, though some people prefer digital envelope apps that charge a similar modest monthly fee. Automated app-based budgeting tends to sit at the higher end of the cost range, since it typically requires a premium subscription to unlock full transaction categorization and real-time alerts.

The real cost across every method is time, particularly during setup. Expect a few hours upfront to review past spending and structure your categories, regardless of which method you choose.

Zero-Based Budgeting vs Pay-Yourself-First vs App-Based Automatic Budgeting: Which One Is Right for You?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Zero-Based Budgeting | Detail-oriented planners who want full visibility | Maximum control, with every dollar assigned a clear job | Time-intensive and can feel overwhelming for beginners |

| Pay-Yourself-First Budgeting | People who prioritize savings over detailed tracking | Simple, automated, and low-maintenance once set up | Offers little visibility into where discretionary money actually goes |

| App-Based Automatic Budgeting | Tech-comfortable users who want tracking without manual entry | Automatic categorization and real-time overspending alerts | Usually requires a paid subscription for full functionality |

Who Should Actually Care About Choosing the Right Budgeting Method?

This matters for anyone who's tried and abandoned a budget before, since the method itself, not a lack of discipline, is often the real reason it failed. It's especially relevant for people with irregular income who need more flexibility than a rigid method allows, and for households trying to align two different money personalities under one shared system.

Mistakes Most People Make

A handful of habits lead people to pick the wrong method and then blame themselves when it fails.

Choosing the most detailed method available because it seems most "serious" about money often backfires for people who dislike manual tracking. Starting with a simpler method and adding structure later usually works better than starting too rigid.

Assuming one partner's preferred method will automatically work for a shared household budget ignores that different money personalities need to be reconciled deliberately. Discussing preferences openly before choosing a shared system avoids ongoing friction.

Switching methods every time one feels difficult, rather than giving it a few months to become habitual, prevents any system from ever feeling automatic. Committing to at least one full budgeting cycle before judging a method's fit gives a fairer test.

Ignoring irregular expenses regardless of which method is chosen leads to the same problem across every system: treating predictable but infrequent costs as unexpected emergencies. Building a sinking fund category into any method smooths this out.

What Most Articles Won't Tell You

Most budgeting guides present these methods as mutually exclusive, but the strongest real-world systems are often hybrids. Automating savings through a pay-yourself-first approach while tracking discretionary spending loosely with 50/30/20 percentages captures the strengths of both without the full time commitment of either alone.

There's also a detail worth knowing: your ideal method can change as your life changes. Someone who thrived with detailed zero-based budgeting while paying off debt aggressively may prefer a more automated, hands-off system once that debt is gone and the urgency fades.

Advanced Moves Worth Knowing

Running a short trial period, just two to three weeks, with a new method before fully committing lets you catch a poor fit early without having wasted months on a system you'll likely abandon anyway.

Building in a small "no questions asked" discretionary category, regardless of which core method you choose, tends to improve long-term adherence by removing the all-or-nothing pressure that causes people to quit after one indulgent purchase.

Frequently Asked Questions

Which budgeting method is easiest for a complete beginner?

The 50/30/20 method is generally the easiest starting point, since it uses broad percentage categories rather than requiring detailed tracking of every individual transaction right away.

Can I combine more than one budgeting method?

Yes, and many people find hybrids work better than any single method alone. A common combination pairs pay-yourself-first automation for savings with a looser percentage-based framework for everyday spending.

Is envelope budgeting still practical if I mostly use a debit or credit card?

Yes, many budgeting apps now offer digital envelope features that replicate the physical cash system electronically, letting you cap spending per category without carrying actual cash.

How long should I try a budgeting method before deciding it doesn't work?

Give it at least one full budgeting cycle, typically a month, and ideally two to three months before judging fit, since the first few weeks of any new system tend to feel unfamiliar regardless of how well it ultimately suits you.

Do I need a budgeting app, or can I use one of these methods manually?

Every method described here can be run manually with a spreadsheet or notebook at no cost. An app simply adds convenience through automatic transaction categorization, which some people find worth paying for and others don't need at all.

The Bottom Line on Budgeting Methods in 2026

There's no universally best budgeting method, only the one that matches how your brain actually works around money. Detail-oriented planners tend to thrive with zero-based or envelope budgeting, while automation-lovers do better with pay-yourself-first or reverse budgeting. Try one for a full cycle before judging it, and don't be afraid to combine methods or switch as your financial priorities shift. The right system is the one still running on autopilot a year from now.

Read Next

Shock Alert: Major Federal Student Loan Changes Set for July 2026!

Shocking Reveal: Why a Major Lender Isn't Fearful of Surging Auto Prices

Warning: HELOC Rates Surge as 'Equity-Rich' Homeowner Numbers Collapse!

USDA's Shocking Loan Assistance: Drought Crisis Hits Nebraska Hard!

Shock Move: Houston Dynamo’s Logan Erb Loaned to Corpus Christi FC