High-Yield Savings Accounts 2026: Best Rates & How to Pick

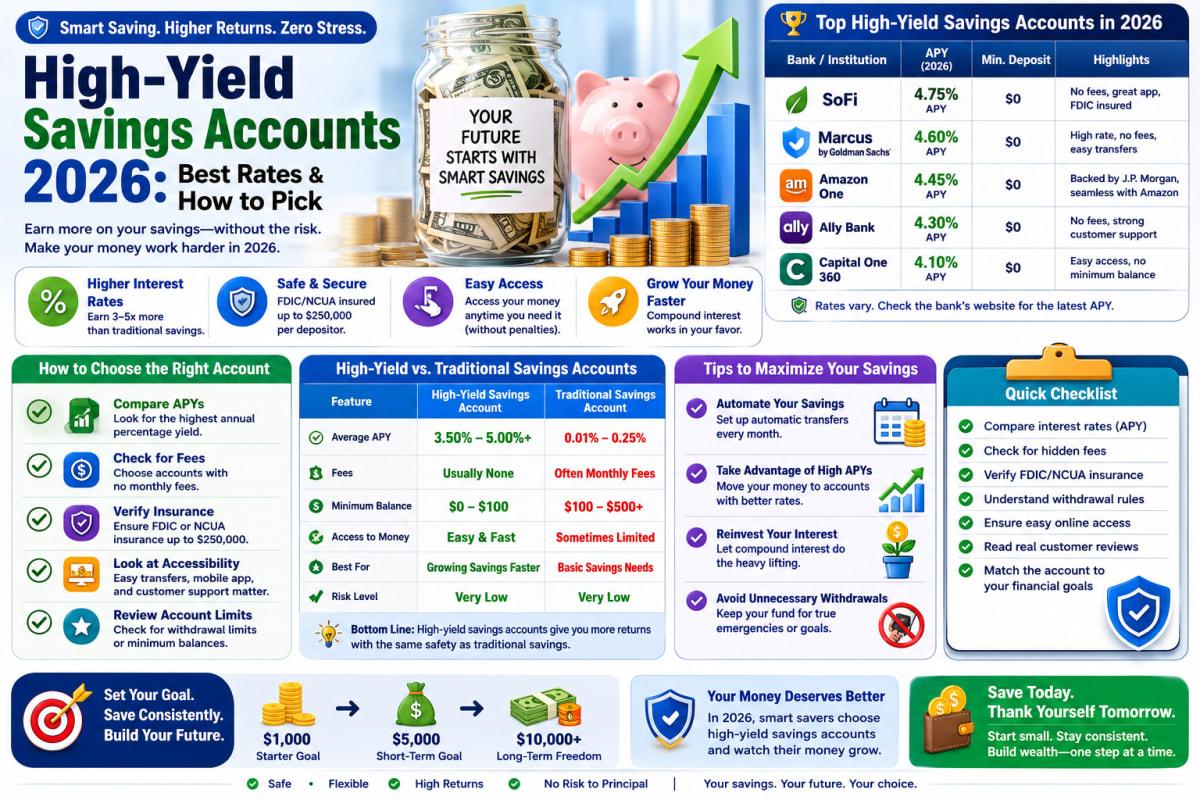

Top high-yield savings rates are hitting up to 5% APY in 2026, nearly 13 times the national average. Here's how to compare accounts and pick the right one.

High-Yield Savings Accounts 2026: Best Rates & How to Pick

Most traditional bank savings accounts are still paying close to nothing, while the best high-yield accounts are earning up to 5% APY right now. On a $10,000 balance, that gap alone is worth hundreds of dollars a year sitting on the table.

High-yield savings accounts have become one of the simplest ways to earn real returns on cash you want to keep safe and accessible. This guide breaks down where rates actually stand in 2026, what separates a genuinely strong account from a mediocre one, and exactly how to choose the right account for your situation, whether you're building an emergency fund or parking cash for a short-term goal.

High-Yield Savings Accounts — What They Are and Why They Matter

A high-yield savings account is a savings account that pays a significantly higher interest rate than the industry average, usually offered by online banks that skip the cost of physical branches and pass those savings on to customers. It's not a separate account category, just a savings account with a notably better rate.

The difference between a standard savings account and a high-yield one can mean earning ten to thirteen times more interest on the exact same balance, with no added risk since these accounts remain fully FDIC or NCUA insured up to standard limits.

Why This Is Important Right Now

Picture someone with $25,000 sitting in a big-bank savings account earning close to nothing, while a comparable online account could be earning close to $1,000 more per year on that same balance. That gap exists purely because switching banks feels like a hassle, not because of any real barrier.

The Federal Reserve has held its benchmark rate steady through multiple meetings in 2026 after several cuts in late 2025, which means savings rates have stabilized at levels still well above what most traditional banks offer. That makes now a genuinely good window to lock in a strong rate before any future rate movement changes the picture.

Key Facts About High-Yield Savings Accounts

A few core facts explain how these accounts work and why the rate gap is so large right now. These set the foundation for comparing your options.

- Top rates are currently reaching up to around 5% APY — compared to the FDIC's national average of roughly 0.38% for standard savings accounts.

- Most competitive accounts charge no monthly fee and no minimum balance — making it easy to open one with a small starting deposit.

- Rates are variable, not locked in — they can rise or fall based on Federal Reserve rate decisions, unlike a fixed-rate CD.

- FDIC or NCUA insurance covers up to $250,000 per depositor — confirming this coverage before opening an account is a simple but essential step.

- Interest earned is taxable as ordinary income — your bank issues a 1099-INT for any interest earned above $10 in a year.

What the Industry Data Shows

Industry data suggests that the gap between brick-and-mortar bank rates and the best online high-yield rates is wider than it's been in roughly a decade, largely because online banks continue undercutting traditional institutions on overhead costs while competing aggressively for deposits.

Coverage from outlets like Bankrate, NerdWallet, and Forbes Advisor has consistently tracked rates trending slightly downward since early June 2026, even as a handful of banks bucked that trend and raised their rates to stay competitive. That mixed movement suggests the market remains competitive enough to reward comparison shopping rather than settling for whichever account is most heavily advertised.

Benefits and Real Opportunities

Choosing a strong high-yield account creates real, measurable value with essentially no added risk compared to a standard savings account.

- Meaningfully higher returns — the difference between a top rate and a typical bank rate can add up to hundreds of dollars a year on a modest balance.

- No added risk — FDIC or NCUA insurance protects your principal the same way it does at any traditional bank.

- Full liquidity — your money remains accessible within a day or two, unlike a CD or investment account.

- Useful savings tools — many top accounts now offer features like automatic savings buckets or goal-tracking built into their app.

Costs and What to Expect

Most competitive high-yield savings accounts charge no monthly maintenance fee and require no minimum opening deposit, though a handful of accounts require a minimum balance, sometimes around $5,000, to earn their highest advertised rate. Falling below that threshold on tiered accounts typically drops you to a much lower rate rather than triggering a fee.

Some combined checking-and-savings products require you to meet specific conditions, like setting up direct deposit or maintaining a minimum average daily balance, to unlock their top APY. Without meeting those conditions, your rate can drop dramatically, sometimes below 1%, so it's worth reading the requirements closely rather than assuming the advertised headline rate applies automatically.

Interest earned is taxed as ordinary income at your federal marginal rate and most state rates, which is worth factoring into your expectations, especially on a larger balance.

High-Yield Savings Account vs Money Market Account vs Cash Management Account: Which One Is Right for You?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| High-Yield Savings Account | Most savers wanting simplicity and top rates with no strings attached | Fewer balance tiers and no check-writing requirements to worry about | Rates are variable and can drop with future Fed rate cuts |

| Money Market Account | People who occasionally need to write checks against their savings | Comparable APYs to HYSAs with added check-writing flexibility | May require a higher minimum balance to earn the top rate |

| Cash Management Account | Investors who want savings and brokerage-style features in one place | Competitive rates alongside easy transfers into investment accounts | Usually offered through investment platforms rather than traditional banks |

Who Should Actually Care About High-Yield Savings Accounts?

This matters for anyone keeping cash in a traditional bank savings account earning close to nothing, whether that's an emergency fund, savings for a big purchase, or money set aside for a short-term goal. It's especially relevant for people who assume switching banks is complicated, since most online high-yield accounts can be opened in under fifteen minutes.

Mistakes Most People Make

A handful of habits keep people from actually earning what these accounts advertise.

Assuming your current bank's savings rate is competitive without ever checking leads many people to leave hundreds of dollars in interest unclaimed each year. Comparing your current rate against current top offers takes just a few minutes and often reveals a meaningful gap.

Chasing the single highest advertised APY without checking the requirements to earn it can backfire, especially on combined checking-and-savings accounts that require direct deposit or a minimum balance. Reading the qualifying conditions first avoids landing on a much lower rate than expected.

Opening an account without confirming FDIC or NCUA insurance is a rare but serious mistake. Verifying this directly on the bank's website before depositing any funds is a simple, essential step.

Assuming a high-yield account is a place to invest for growth misunderstands its purpose. This money should stay liquid and safe, not treated as a substitute for long-term investing.

What Most Articles Won't Tell You

Most roundups focus on the single highest headline rate, but tiered-rate accounts often mean you need a specific minimum balance, sometimes $5,000 or more, to actually earn that top APY. Below that threshold, your effective rate can be far lower than advertised.

There's also a detail worth knowing: rates have been trending slightly downward at some banks since early June 2026 even while a few institutions increased theirs to stay competitive. That means the "best" account can shift within weeks, so checking current rates before opening an account matters more than relying on outdated best-of lists.

Advanced Moves Worth Knowing

Splitting savings across a no-minimum HYSA for your accessible emergency cushion and a higher-tier account requiring a larger balance for longer-term cash can capture the best of both worlds without sacrificing liquidity where it matters most.

Setting a recurring quarterly reminder to compare your account's rate against current top offers ensures you're not quietly earning a below-market rate if your bank lowers its APY without much notice.

Frequently Asked Questions

Are high-yield savings accounts actually safe?

Yes, as long as the account is FDIC-insured or NCUA-insured, your principal is protected up to $250,000 per depositor, the same protection as any traditional bank account.

Why do online banks offer higher rates than traditional banks?

Online banks avoid the overhead cost of physical branches, which allows them to pass more of that savings on to customers in the form of higher interest rates.

Do I have to pay taxes on high-yield savings account interest?

Yes, interest earned is taxed as ordinary income at your federal marginal rate and most state rates. Your bank will issue a 1099-INT if you earn more than $10 in interest during the year.

Can a high-yield savings account rate change after I open it?

Yes, these rates are variable, not fixed, and typically move in response to Federal Reserve rate decisions. A rate you open an account at today isn't guaranteed to stay the same over time.

Is a high-yield savings account better than a CD for an emergency fund?

Generally, yes. A high-yield savings account keeps your money fully liquid, while a CD locks it up for a set term and often charges a penalty for early withdrawal, which makes it a poor fit for money you might need on short notice.

The Bottom Line on High-Yield Savings Accounts in 2026

High-yield savings accounts in 2026 offer a genuinely simple way to earn meaningfully more on your cash without taking on any added risk. The gap between the best rates and what most traditional banks pay is wide enough that switching is almost always worth the fifteen minutes it takes. Compare your current rate against today's top offers, confirm the account is properly insured, and move your savings if the math makes sense. Your money should be working at least as hard as you did to save it.

Read Next

Oil Surges as Trump Rejects Iran Offer: Market Crisis Looms!

Top Investor Warns: AMD Stock Collapse Makes No Sense!

Palantir Stock Plummets: What’s Causing This Urgent Revenue Crisis?

Shock CPI Data and Retail Sales Surge: What It Means for Your Wallet

Stocks on Edge: Will Key Players Surge to Record Highs?