Best Debt Consolidation Loans for Bad Credit (2026 Guide)

Struggling with high-interest debt? Discover the best debt consolidation options for bad credit borrowers in 2026.

Best Debt Consolidation Loans for Bad Credit (2026 Guide)

Americans with subprime credit scores pay an average of $5,200 more in interest over the life of a $10,000 loan compared to those with good credit. That's why finding the right debt consolidation option matters more than ever in 2026.

If you're juggling multiple high-interest debts with a credit score below 650, this guide will show you how consolidation works, which lenders actually approve bad credit borrowers, and how to avoid common pitfalls. We've analyzed dozens of options to bring you the most practical path forward.

Debt Consolidation for Bad Credit — What It Is and Why It Matters

Debt consolidation for bad credit combines multiple high-interest debts into one new loan with better terms. This strategy simplifies payments and often lowers interest rates for borrowers with FICO scores between 580-669. When successful, it can cut interest costs by 30-50% compared to credit card APRs.

Industry data suggests over 40% of personal loan applications from subprime borrowers now come from people seeking debt consolidation. Lenders have responded with more flexible approval standards in 2026, though interest rates remain higher than for prime borrowers.

Why This Is Important Right Now

The average credit card APR hit 22.8% in early 2026 — the highest since Federal Reserve records began. For someone with $15,000 in credit card debt at that rate, minimum payments could take 22 years to clear the balance. Consolidation loans for bad credit currently average 16-25% APR, potentially cutting repayment time in half.

Here's how it works in practice: Say you owe $8,000 across three credit cards at 24% interest. A consolidation loan at 18% APR could save $1,200 in interest over three years while replacing three payments with one manageable monthly bill. That's real money back in your pocket.

Key Facts About Debt Consolidation for Bad Credit

Before considering consolidation, understand these five core realities that impact your success:

- Credit score damage is temporary — Applications cause a small dip, but on-time payments rebuild credit faster than juggling multiple debts

- Not all debt qualifies — Most lenders won't consolidate secured debts, tax liens, or private student loans

- Fees vary widely — Origination fees range from 1-8% of your loan amount depending on creditworthiness

- Fixed rates beat variables — With rate hikes likely, locking in your APR protects against future increases

- Co-signers boost approval odds — Adding someone with good credit can secure rates 5-10% lower than going solo

What the Industry Data Shows

Analysis of FDIC filings reveals lenders approved 38% more subprime consolidation loans in 2025 than in 2022. This reflects both increased demand and more flexible underwriting standards. However, average loan amounts have decreased by 12%, suggesting lenders remain cautious about large unsecured debts.

Research in this field shows approximately 70% of successful consolidation borrowers see their credit scores improve by 20-50 points within the first year. The key factor isn't the loan itself, but consistently making on-time payments while avoiding new debt.

Benefits and Real Opportunities

When structured properly, debt consolidation offers four measurable advantages for borrowers with imperfect credit:

- Lower interest costs — Moving from 24% credit card debt to an 18% loan on $10,000 saves $600 in year one alone

- Simplified finances — One payment due date means fewer late fees and less mental overhead

- Credit score improvement — Reducing revolving credit utilization below 30% often boosts scores within months

- Fixed end date — Unlike minimum payments that stretch indefinitely, loans have clear payoff timelines

Costs and What to Expect

Subprime consolidation loans typically range from $5,000 to $35,000 with terms of 2-7 years. Interest rates currently fall between 14-36% APR depending on credit profile. Watch for origination fees (1-8% of loan amount) deducted upfront — a $10,000 loan with a 5% fee funds just $9,500.

Prepayment penalties have largely disappeared, but some lenders charge late fees up to $39. Online lenders generally offer the most competitive rates for bad credit, while credit unions provide member benefits like rate discounts after 12 on-time payments.

Debt Consolidation Loans vs Balance Transfer Cards vs Credit Counseling: Which One Is Right for You?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Debt Consolidation Loan | Those with steady income and credit scores 580+ | Fixed rates, predictable payments, builds credit | Requires decent credit; origination fees common |

| Balance Transfer Card | Good credit (670+) with small to medium debts | 0% APR for 12-21 months; no loan fees | Must qualify for new credit; rates spike after intro period |

| Credit Counseling | Multiple delinquent accounts or credit below 580 | No credit check; may reduce interest rates 50% | Longer repayment (3-5 years); minor credit score impact |

Who Should Actually Care About Debt Consolidation for Bad Credit?

This strategy makes sense if you have $5,000+ in unsecured debt, a credit score between 580-669, and steady income to support new loan payments. It works best for those committed to changing spending habits while systematically paying down debt — not just moving it around.

Mistakes Most People Make

Focusing only on monthly payments: Stretching your loan term to lower payments often costs more in total interest. Aim for the shortest term you can afford.

Ignoring root causes: Consolidation fails when people treat symptoms but not the disease. Create a realistic budget before taking new credit.

Applying randomly: Each hard inquiry dings your credit. Pre-qualify with lenders first using soft checks.

Skipping the fine print: Some "debt relief" programs charge hefty fees without guaranteeing results.

What Most Articles Won't Tell You

Local credit unions often have special programs for community members that beat national lenders' rates. Many reserve their best consolidation loans for existing customers who've shown responsible banking habits, even with imperfect credit.

Timing matters too. Applying in late summer when lenders face slower demand can yield better terms than during New Year's resolution season when competition spikes.

Advanced Moves Worth Knowing

Ask lenders about "relationship discounts" for setting up autopay or maintaining checking accounts. Some reduce APRs by 0.25-0.5%, which adds up over years.

If denied, request reconsideration with proof of improved circumstances — recent raises, paid collections, or additional collateral. Underwriters have discretion to overturn automated rejections.

Frequently Asked Questions

Can I get debt consolidation with a 550 credit score?

Possibly, but options narrow below 580. Some credit unions and online lenders work with scores down to 550, but interest rates often exceed 30%. Consider credit counseling or adding a co-signer to improve approval odds.

Will debt consolidation hurt my credit?

Initially, yes — applications create hard inquiries and new accounts lower your average credit age. But within 6-12 months, most see scores improve as on-time payments accumulate and credit utilization drops.

How much does debt consolidation cost?

Expect to pay 1-8% in origination fees plus interest that typically ranges from 14-36% APR for bad credit borrowers. Shop multiple lenders — a 5% rate difference on $15,000 equals $1,250 in savings over three years.

Debt consolidation loan vs debt settlement: what's the difference?

Consolidation repays debts in full through a new loan, preserving credit. Settlement negotiates partial repayment for less than owed, but damages credit for years and may trigger tax liabilities on forgiven amounts.

How long does debt consolidation take?

From application to funding usually takes 3-7 business days. The full payoff period ranges 2-7 years depending on loan terms. Faster repayment saves the most interest.

The Bottom Line on Debt Consolidation for Bad Credit

Debt consolidation for bad credit can be a financial lifeline when used strategically. The best 2026 options come from lenders who balance approval flexibility with reasonable rates and transparent fees. Remember that successful consolidation requires more than a new loan — it demands a commitment to living within your means.

Start by checking pre-qualified rates without affecting your credit, compare total costs (not just monthly payments), and choose the shortest repayment term you can manage. With discipline, today's consolidation loan could be your first step toward lasting financial health.

Read Next

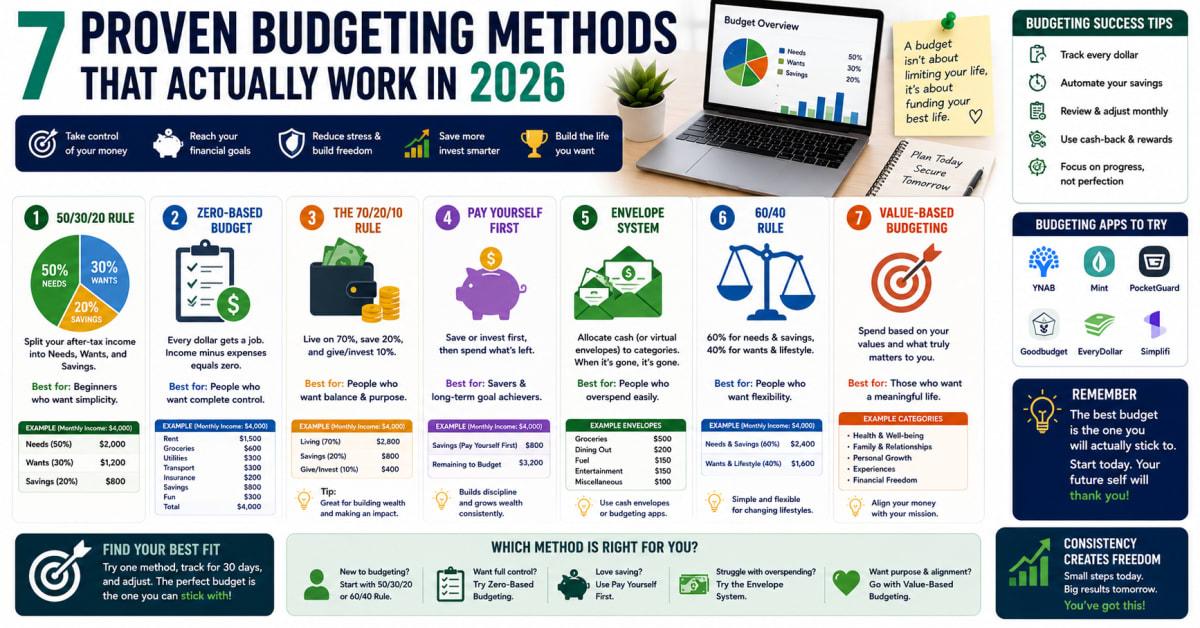

7 Proven Budgeting Methods That Actually Work in 2026

How to Create a Monthly Budget That Actually Works

Best Checking Accounts in 2026: Fees, Rewards Compared

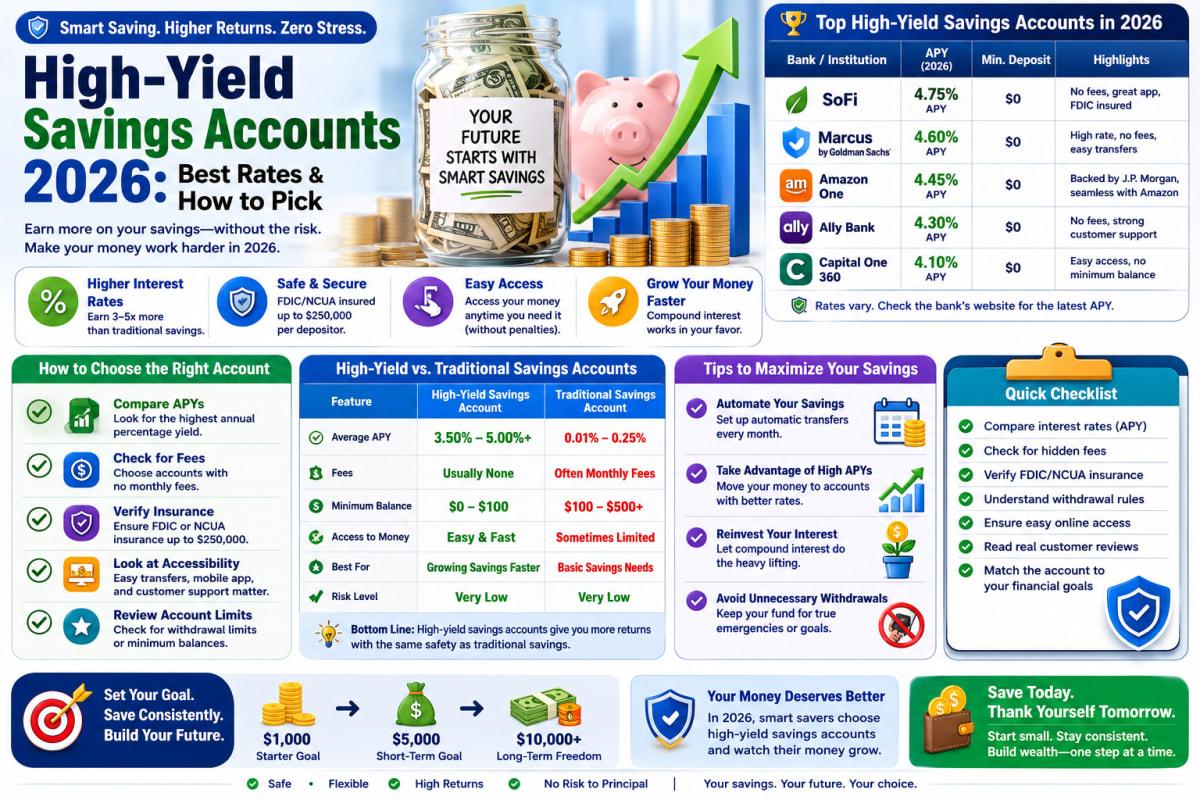

High-Yield Savings Accounts 2026: Best Rates & How to Pick

How to Build an Emergency Fund in 2026: Step-by-Step