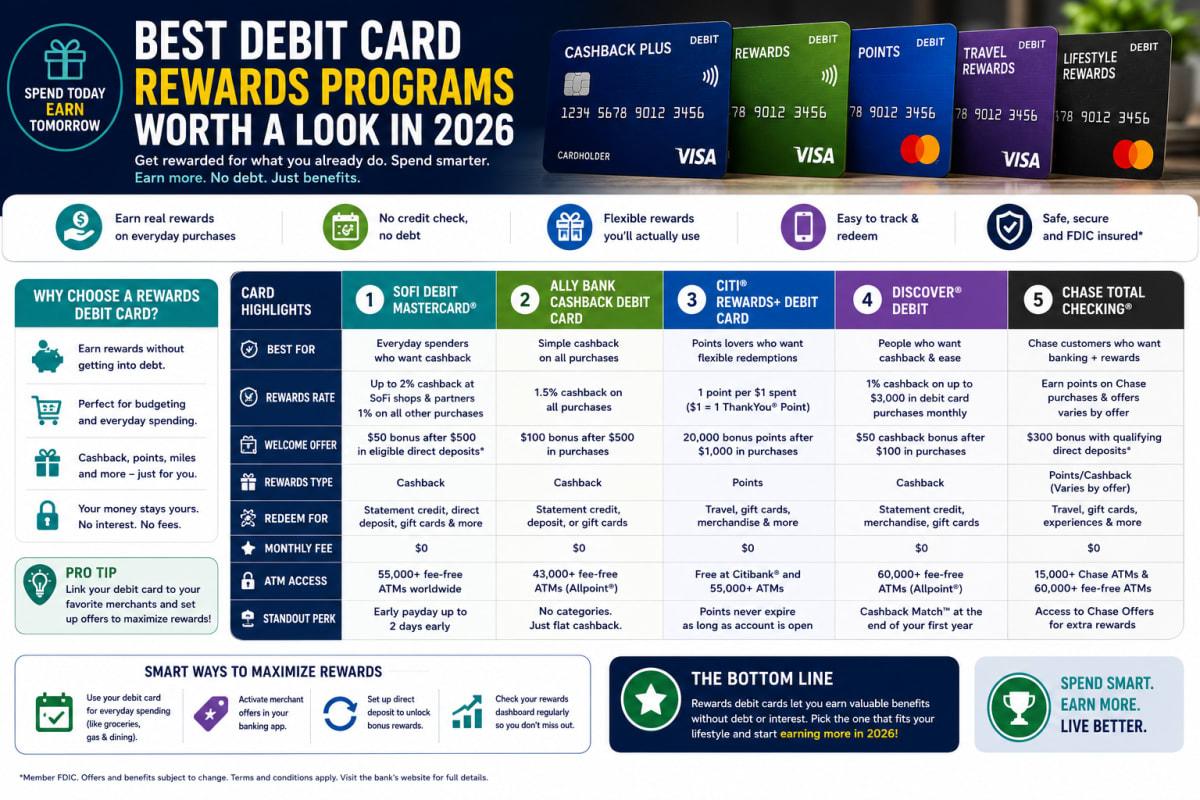

Best Debit Card Rewards Programs Worth a Look in 2026

Debit card rewards are rarer than credit card perks, but a handful of programs actually pay real cash back with no annual fee and no interest risk.

Best Debit Card Rewards Programs Worth a Look in 2026

Most people assume rewards only come from credit cards. That assumption costs them money, because a small but growing group of debit card programs now pay real cash back on everyday spending.

Debit card rewards programs work differently than credit card rewards, and the gap between the best and worst options is bigger than most people expect. This guide breaks down how these programs actually pay out, what fees to watch for, and how to tell a genuinely useful rewards debit card from one that looks good only in the fine print.

Debit Card Rewards Programs — What They Are and Why They Matter

Debit card rewards programs return a percentage of your spending, or occasionally points, when you use a debit card linked to a checking account. Unlike credit cards, there's no borrowing involved and no interest to worry about, since the money spent is already yours.

These programs matter because they let disciplined spenders earn value from everyday purchases without any risk of accumulating debt, which makes them a genuinely different tool than a rewards credit card, not just a lesser version of one.

Why This Is Important Right Now

Picture someone who avoids credit cards entirely out of caution but still wants to get something back for their everyday spending. Without knowing which banks actually offer meaningful debit rewards, they end up leaving money on the table simply because most traditional checking accounts don't advertise this option clearly.

Federal Reserve survey data shows debit cards are now a leading choice for in-person purchases, which means the spending base for these rewards programs keeps growing even as credit card rewards get most of the attention.

Key Facts About Debit Card Rewards Programs

A few core facts explain how these programs actually function and where the real value sits. Understanding this upfront saves you from comparing apples to oranges.

- Cash back rates typically range from 1% to 5% — with the higher end usually reserved for specific spending categories.

- Signature transactions often qualify, PIN transactions may not — many programs only reward purchases processed as credit rather than PIN-based debit.

- Monthly or annual spending caps are common — rewards above the cap often drop to a lower rate or stop entirely.

- Some programs charge a monthly fee for higher rewards tiers — meaning the advertised top rate isn't always the free, default option.

- Using a debit card doesn't build credit history — rewards or not, these purchases have no impact on your credit score.

What the Industry Data Shows

Industry data suggests that consumer interest in earning rewards without taking on debt has grown steadily, with some newer banking programs explicitly marketing debit rewards as a way to reward spending money you already have. That framing has resonated enough that several fintech and traditional banks have expanded their debit rewards offerings in response.

Coverage from outlets like U.S. News and CNBC has consistently noted that while debit rewards remain less generous overall than credit card rewards, certain standout programs, particularly ones tied to points-per-dollar structures with no cap, can rival mid-tier credit card value for the right spender.

Benefits and Real Opportunities

A well-chosen debit rewards program offers a different kind of value than credit card rewards, built around simplicity and zero debt risk.

- No interest risk — you're spending your own money, so there's no way to erase your rewards with interest charges.

- No credit check required — most debit rewards programs are tied to a checking account rather than a credit application.

- Good fit for disciplined budgeters — since you can't spend more than what's in your account, rewards come without overspending temptation.

- Some programs pair rewards with high-yield checking — letting you earn both cash back and interest on your balance in one account.

Costs and What to Expect

Many of the strongest debit rewards programs charge no monthly fee at all, particularly newer digital-first checking accounts competing for everyday spenders. Others, especially those offering cash back through curated merchant deals, may require a specific account tier with a monthly fee ranging from a few dollars up to around $25, depending on features.

Spending caps are one of the most important cost considerations, since a program advertising 5% back might only apply that rate up to a monthly cap, often a few thousand dollars, before dropping to a much lower rate. Some cash back programs also require exceeding a minimum non-PIN spending threshold each month before any rewards apply at all, which can catch new users off guard.

Foreign transaction fees on debit purchases abroad vary by issuer, so frequent travelers should check this separately from the rewards structure itself.

Flat Point-Per-Dollar Programs vs Merchant-Deal Cash Back vs High-Yield Rewards Checking: Which One Is Right for You?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Flat Point-Per-Dollar Programs | People who want simple, uncapped earning on every purchase | No cap on points earned, with no monthly fees on many accounts | Point value often lower than a straightforward cash back percentage |

| Merchant-Deal Cash Back | Shoppers willing to browse and opt into specific retailer deals | Cash back rates can be high at participating merchants | Requires actively opting into deals and often carries a monthly account fee |

| High-Yield Rewards Checking | People who want cash back plus interest on their balance | Combines spending rewards with a competitive APY on your balance | May have minimum balance or direct deposit requirements to qualify |

Who Should Actually Care About Debit Card Rewards Programs?

This matters most for people who prefer to avoid credit cards entirely, whether by choice or because they're rebuilding credit and want to avoid new debt. It's also relevant for disciplined budgeters who already live within a strict spending plan and want to earn something extra from purchases they'd make regardless.

Mistakes Most People Make

A few common errors keep people from getting real value out of these programs.

Running every purchase as a PIN transaction because it feels more secure can accidentally disqualify you from rewards that only apply to signature-based purchases. Checking your specific program's requirements before defaulting to PIN avoids this loss.

Choosing a card based purely on the advertised top cash back rate, without checking the monthly cap, leads to disappointment once spending exceeds that threshold. Estimating your typical monthly spend against the cap before committing avoids the mismatch.

Paying a monthly fee for a premium rewards tier without calculating whether your spending actually earns enough to offset it can quietly cost you money instead of earning it. Running the math on your typical spending first prevents that trap.

Assuming all rewards checking accounts are equally safe skips an important check: confirming the account is genuinely FDIC-insured before depositing significant funds.

What Most Articles Won't Tell You

Most roundups focus heavily on the advertised cash back percentage, but redemption speed and flexibility matter just as much. Some programs credit rewards to your account balance automatically each month, while others require manual redemption or limit you to gift cards, which changes how usable the rewards actually are.

There's also a lesser-known category worth understanding: some accounts reward you for banking behavior itself, like maintaining a balance or setting up direct deposit, rather than for spending. Pairing one of these with a separate spending-based debit rewards card can capture value from both sides of your finances at once.

Advanced Moves Worth Knowing

Pairing a high-yield rewards checking account for your main balance with a separate merchant-deal debit card for discretionary spending lets you capture interest and cash back simultaneously without paying for two full-fee accounts.

Checking whether your bank periodically rotates or expands its merchant-deal categories can reveal opportunities to boost your effective rewards rate during specific months without switching accounts at all.

Frequently Asked Questions

Are debit card rewards as good as credit card rewards?

Generally not, no. Debit rewards tend to be lower and more limited by caps or fees, though a handful of standout programs offer uncapped points or cash back that come reasonably close to mid-tier credit card value.

Does using a rewards debit card build my credit score?

No, debit card spending, rewards or not, doesn't get reported to credit bureaus and has no effect on your credit score, since there's no borrowing involved.

Do debit card rewards programs charge fees?

It depends on the program. Many no-fee checking accounts offer basic cash back or points, while some premium merchant-deal programs require a monthly account fee to access the highest rewards tiers.

Can I have a rewards debit card and a rewards credit card at the same time?

Yes, and many people do exactly that, using a debit card for discretionary or budgeted spending and a credit card for larger purchases they pay off in full each month to maximize combined rewards.

What's the easiest type of debit rewards program for a beginner?

Flat point-per-dollar or straightforward cash back programs with no monthly fee are usually easiest for beginners, since there's nothing to activate or track compared to merchant-deal or rotating category programs.

The Bottom Line on Debit Card Rewards Programs

Debit card rewards programs won't outpace top credit card offers, but the best ones give you real value with zero debt risk and no interest to worry about. Look past the headline percentage and check the fee structure, spending caps, and redemption process before committing. If you already prefer debit for daily spending, it's worth checking whether your current bank offers a rewards program you haven't activated yet — you might already be earning less than you could be.

Read Next

Intel Stock Surges After Shocking Chip Deal with Apple!

Nvidia Stock Surges to Record Highs Amid AI Boom – What’s Next?

Lumentum's Stock Soars: What This Hot Index Reveal Means for You

Shock Layoffs: Cloudflare Cuts 1,100 Jobs as Stock Takes a Hit!

Shock Surges: Nasdaq and S&P 500 Record Highs Amid Iran Hopes