Best Cash Back Credit Cards of 2026 Compared

The top cash back credit cards of 2026, compared by rewards structure, fees, and who each one actually fits best.

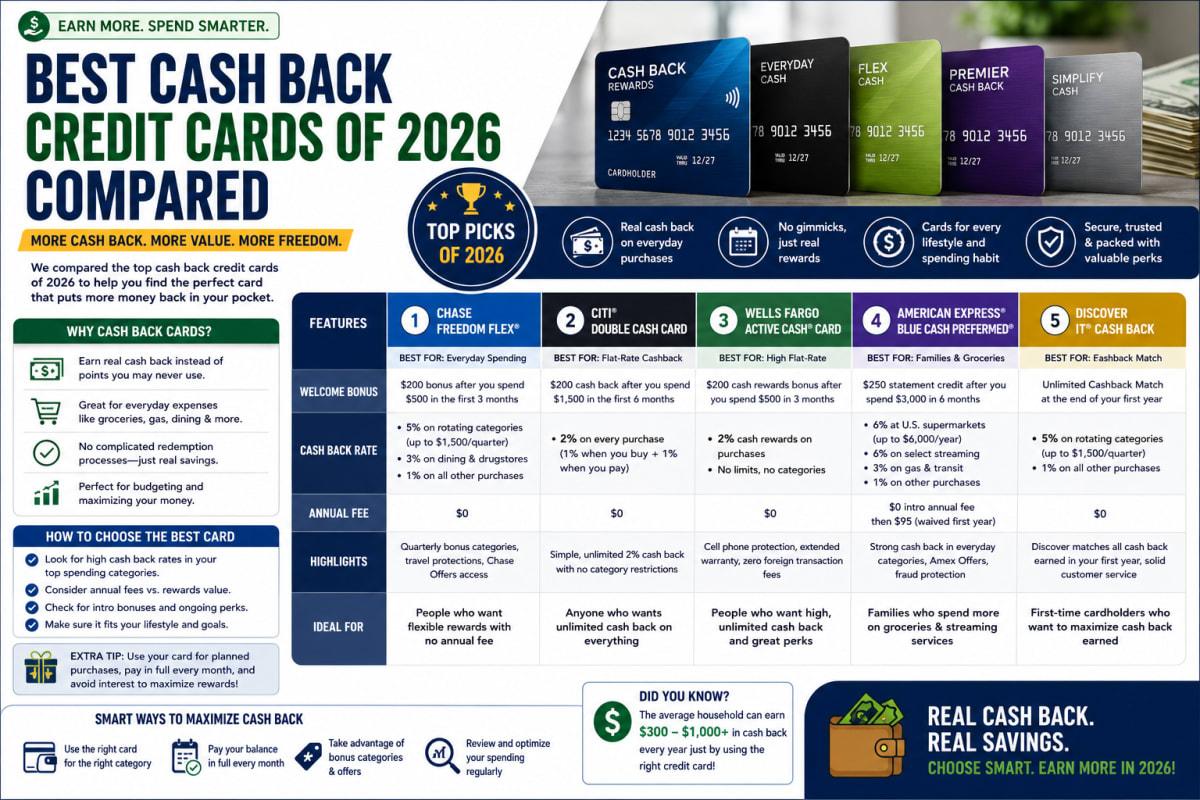

Best Cash Back Credit Cards of 2026 Compared

A cash back card sounds simple until you're staring at five options with different bonus categories, caps, and fine print. The right one depends entirely on how you actually spend, not which card has the flashiest advertised rate.

This roundup of the best cash back credit cards of 2026 breaks down flat-rate, rotating-category, and choice-category cards side by side, so you can match a card to your real spending habits instead of chasing a headline percentage that might not apply to most of your purchases. We'll cover what each type actually pays out, the costs to watch for, and how to avoid the mistakes that quietly cancel out your rewards.

Best Cash Back Credit Cards — What They Are and Why They Matter

Cash back credit cards return a percentage of your spending as a reward, either at a flat rate on everything or at higher rates in specific bonus categories. Some require activation each quarter, others apply automatically, and the difference in effort required can meaningfully affect how much you actually earn.

Choosing well matters because the gap between a mediocre card and a great one, for your specific spending pattern, can add up to hundreds of dollars a year in rewards you'd otherwise leave on the table.

Why This Is Important Right Now

Picture someone who signed up for a rotating-category card years ago and never activates the quarterly bonuses, quietly earning the base 1% rate instead of the 5% they thought they were getting. That gap between advertised and actual rewards is common, and it usually goes unnoticed for years.

With more issuers competing for cardholders in 2026, welcome bonuses and bonus category rates have become more generous, but also more varied. That makes comparing structures carefully more valuable than it's been in a while.

Key Facts About Best Cash Back Credit Cards

Before comparing specific cards, it helps to understand the three basic reward structures that nearly every cash back card falls into. This framework makes the rest of the comparison much easier to follow.

- Flat-rate cards pay the same percentage on everything — typically around 1.5% to 2%, with no categories to track or activate.

- Rotating-category cards offer higher rates on a schedule — often 5% in categories that change quarterly, usually capped and requiring activation.

- Choice-category cards let you pick your bonus category — giving cardholders control over which type of spending earns the highest rate.

- Most top cash back cards carry no annual fee — making it easier to hold one long-term without it costing you money to keep.

- Welcome bonuses require meeting a spending threshold — usually within the first three to six months of account opening.

What the Industry Data Shows

Industry data suggests that flat-rate cards tend to perform best for cardholders who put the bulk of their spending on one card without much variation across categories. Rotating and choice-category cards, on the other hand, tend to outperform for cardholders willing to track categories or adjust their spending slightly to capture higher rates.

Comparison sites like NerdWallet and Bankrate have consistently noted that no-annual-fee flat-rate cards remain some of the most awarded options year over year, largely because their simplicity suits the widest range of spending habits without requiring active management.

Benefits and Real Opportunities

Picking the right cash back card creates value well beyond the rewards themselves, especially when paired with disciplined payoff habits.

- Meaningful annual rewards — a well-matched card can return a genuinely useful amount of cash back on everyday spending.

- No cost to hold — most top cash back cards charge no annual fee, so the rewards are pure upside.

- Flexible redemption — cash back typically converts to a statement credit, direct deposit, or check, unlike travel points tied to a specific program.

- Built-in spending visibility — reviewing where your bonus categories land each quarter doubles as a light budgeting check-in.

Costs and What to Expect

Most leading cash back cards carry no annual fee, which is one reason they've become the default recommendation for everyday spenders. Standard variable APRs on these cards commonly range from the high teens into the high twenties, so carrying a balance can erase the value of any rewards earned.

Rotating-category cards typically cap bonus-rate spending at a set quarterly amount, often around $1,500, with a lower flat rate applying beyond that cap. Choice-category cards often cap their highest rate at a lower quarterly spending threshold too, so it's worth checking the fine print rather than assuming the advertised rate applies to unlimited spending.

Balance transfer fees, where relevant, typically start around 3% during an introductory period and rise afterward, which matters if you're considering one of these cards partly for debt consolidation.

Flat-Rate Cards vs Rotating-Category Cards vs Choice-Category Cards: Which One Is Right for You?

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Flat-Rate Cards (e.g., Wells Fargo Active Cash) | People who want simplicity with no categories to track | Consistent 2% back on every purchase, no activation needed | Lower ceiling compared to bonus-category rates elsewhere |

| Rotating-Category Cards (e.g., Discover it Cash Back) | People willing to activate categories each quarter for higher rates | Up to 5% back in rotating categories, often with a first-year match | Requires quarterly activation and has spending caps on bonus rates |

| Choice-Category Cards (e.g., Bank of America Customized Cash Rewards) | People with one dominant spending category, like dining or online shopping | Lets you pick and switch your top-earning category monthly | Bonus rate is capped on a limited quarterly spending amount |

Who Should Actually Care About Best Cash Back Credit Cards?

This matters for anyone who pays their balance in full every month and wants their everyday spending to work harder. It's especially relevant for first-time cardholders looking for a simple no-fee option, and for experienced users willing to juggle two or three cards to maximize rewards across different spending categories.

Mistakes Most People Make

A few habits quietly reduce how much cash back people actually earn.

Forgetting to activate rotating bonus categories each quarter means defaulting to the base 1% rate without realizing it. Setting a recurring calendar reminder for activation dates fixes this instantly.

Choosing a card based on the highest advertised rate without checking the spending cap can lead to disappointment once that cap is reached early in the quarter. Estimating your actual monthly spending in that category before applying avoids the mismatch.

Carrying a balance to "earn more rewards" erases the value of cash back almost immediately, since interest charges typically far exceed the rewards earned. Paying in full every cycle is the only way these cards genuinely pay off.

Applying for multiple cash back cards in a short window can trigger several hard inquiries at once. Spacing out applications by a few months protects your score while you still build a stronger rewards lineup over time.

What Most Articles Won't Tell You

Most roundups rank cards by advertised rate alone, but the redemption process matters just as much. Some issuers let you redeem cash back for any amount at any time, while others impose a minimum threshold before you can cash out, which affects how quickly your rewards actually become usable.

There's also a detail worth noting: pairing a flat-rate card with a rotating or choice-category card often outperforms relying on either type alone, since you can default to the flat card outside of active bonus periods and switch in for the bonus card only when it makes sense.

Advanced Moves Worth Knowing

Stacking a choice-category card's monthly-adjustable bonus with a flat-rate card as your default gives you a practical way to capture higher rates without needing to track a full rotating schedule.

Reviewing your card's welcome bonus terms before making a large planned purchase, like a big-ticket appliance or trip, can help you time that purchase to satisfy the spending requirement and capture the bonus in one move.

Frequently Asked Questions

Is a flat-rate cash back card better than a rotating-category card?

Not universally, no. Flat-rate cards suit people who want simplicity and consistent spending across categories, while rotating-category cards can outperform for those willing to track and activate quarterly bonuses.

Do cash back credit cards charge annual fees?

Most of the top cash back cards do not charge an annual fee, which is part of why they're so widely recommended for everyday spending. Some premium rewards variants do carry a fee in exchange for higher earning rates.

How is cash back typically paid out?

Most issuers offer redemption as a statement credit, direct deposit, or mailed check. Some allow redemption for any amount at any time, while others require a minimum balance before you can cash out.

Can you have more than one cash back credit card?

Yes, and many experienced cardholders do, often pairing a flat-rate card with a rotating or choice-category card to maximize rewards across different types of spending.

What credit score do you need for the best cash back cards?

Most top-tier cash back cards require good to excellent credit for approval, though some issuers offer cash back options designed for building or fair credit. Checking your score before applying helps set realistic expectations.

The Bottom Line on Best Cash Back Credit Cards

The best cash back credit cards of 2026 aren't defined by a single winner — they're defined by fit. A flat-rate card rewards simplicity, a rotating-category card rewards attention, and a choice-category card rewards control. Match the structure to your actual spending, not the highest number in an ad, and pay your balance in full every month to keep the rewards genuinely free. Compare your current spending habits against these three structures and see which one you're really leaving money on the table with.

Read Next

Shock Announcement: Education Department’s New Rule Could Surge Student Loan Costs!

Shocking Surge: 12 Commandments of EVDC Revive Ford Stock (NYSE:F)

Rocket Lab Stock Surges After Groundbreaking Launch Contract Shocks Wall Street

Shock Surge: Tech Boom Drives S&P 500 and Nasdaq to Record Highs!

Intel Stock Soars to Record High After Shocking Apple Chip Deal!